Halloween is the one and only time of year when employers and employees alike can dress up and let loose a little more than usual in the office. However, make sure you still follow company policies and procedures especially as far as behavior and dress codes are concerned. Halloween in the workplace allows employees to have fun and gives you the opportunity to interact with your co-workers and upper management on a more casual basis; all while building friendships and teamwork, making everyone more comfortable and productive in the workplace.

Category Archives: Health Care Reform

Social Media and The Workplace

The topic of social media and its effects on the workplace have likely come up in your organization. As a relatively new topic in case-law, social media and its place in the workplace is still unsettled. What can you do to protect yourself as an individual and as an organization?

Job Demands Increase with ACA

Have the changes coming forth with the Affordable Care Act impacted your career? If so, you are not alone. Here are a few careers in which job demands have and will continue to increase, as a result of the ACA.

- Human Resources

- Payroll

- Legal Professionals

- Nurses

- Occupational Therapists

- Personal Trainers

- Customer Service Professionals

- Insurance Consultants

- Medical Billers

- Medical Coders

- Computer Programmers

Are you a stand out professional, technical professional, driver, or skilled worker seeking contingent, temporary, or long term career opportunities? Visit our job board for more information! Want to learn more about how you can gain access to Trillium’s national network of professionals and skilled workers? Contact us today!

Trillium, a national leader in staffing and recruitment is a valued staffing partner to over 5,000 companies nationwide. Trillium is privately owned by Oskar René Poch.

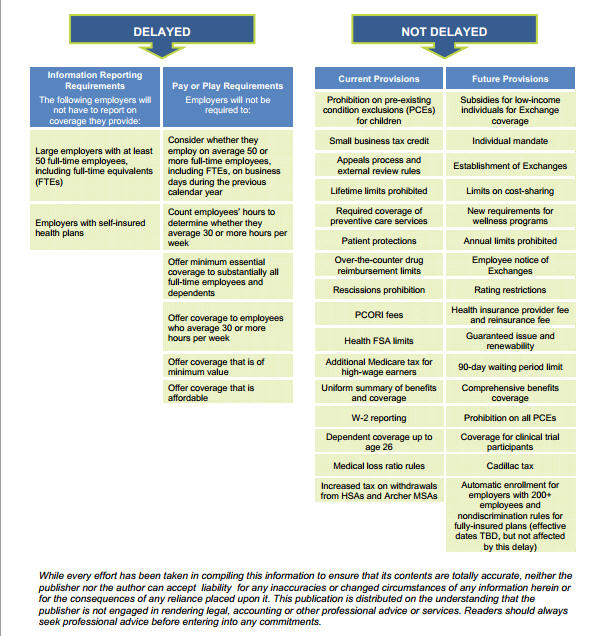

IRS Guidance on Delay of Employer Mandate Penalties and Reporting Requirements

Brought to you by Kapnick Insurance Group

On July 9, 2013, the Internal Revenue Service (IRS) issued Notice 2013-45 to provide formal guidance on the delay of the Affordable Care Act (ACA) large employer “pay or play” rules and related information reporting requirements. The provisions affected by the delay are:

- § 4980H employer shared responsibility provisions;

- § 6055 information reporting requirements for insurers, self-insuring employers and certain other providers of minimum essential coverage; and

- § 6056 information reporting requirements for applicable large employers.

For 2014, compliance with the information reporting rules is completely optional and the IRS will not assess penalties under the pay or play rules. Both the information reporting and the employer pay or play requirements will be fully effective for 2015.

Information Reporting Requirements

The ACA amended the Internal Revenue Code (Code) to require large employers, health insurance issuers and selffunded plan sponsors to report information about health plan coverage to the IRS so that the federal government can enforce the employer mandate.

Code § 6055 requires annual information reporting by health insurance issuers, self-insuring employers, government agencies and other providers of health coverage. Code § 6056 requires annual information reporting by applicable large employers related to the health coverage that the employer offers (or does not offer) to its full-time employees.

Employer Shared Responsibility Requirements

Under the ACA, large employers that do not offer their full-time employees (and dependents) health coverage that is affordable and provides minimum value may be subject to penalties. The ACA’s employer mandate provisions are also referred to as the employer shared responsibility or pay or play rules.

One-Year Implementation Delay

The large employer pay or play rules and related reporting requirements were set to take effect in 2014. However, on July 2, 2013, the Treasury announced that these will be delayed for one year, until 2015. This means that:

- Information reporting under §§ 6055 and 6056 will be optional for 2014 and no penalties will be applied for failure to comply with these requirements for 2014; and

- No employer shared responsibility payments will be assessed for 2014.

However, both the information reporting and the employer pay or play requirements will be fully effective for 2015.

The IRS issued Notice 2013-45 to provide more information on the delay.

According to the IRS, the delay of the reporting requirements provides additional time for input from employers and other reporting entities in an effort to simplify these requirements, consistent with effective implementation of the ACA. This delay is also intended to provide employers, insurers and other providers of minimum essential coverage time to adapt their health coverage and reporting systems.

The delay of the employer mandate penalties was required because of issues related to the reporting requirements. Because the reporting rules were delayed, the Treasury believed it would be nearly impossible to determine which employers owed penalties under the shared responsibility provisions.

The pay or play regulations issued earlier this year left many unanswered questions for employers. The IRS highlighted several areas where it would be issuing more guidance. Presumably, the additional time will give the IRS and Treasury the opportunity to provide more comprehensive guidance on implementing these requirements.

Effect on Other ACA Provisions

The delay does not affect any other provision of the ACA, including individuals’ access to premium tax credits for coverage through an Exchange and the individual mandate.

Individuals will continue to be eligible for the premium tax credit to purchase coverage through an Exchange as long as they meet the eligibility requirements (for example, their household income is within a specified range and they are not eligible for other minimum essential coverage).

Future Guidance

Proposed rules for the information reporting provisions are expected to be published this summer. The proposed rules will reflect the fact that transition relief will be provided for the information reporting requirements.

It is still unclear how the new deadline will impact guidance that has already been issued, such as the transition relief for non-calendar year plans and the optional safe harbor for determining full-time status. Future guidance may affect these and other rules under the ACA.

What This Means for Employers

The Obama Administration’s decision to delay the employer mandate penalties and related reporting requirements will have a significant effect on many employers. See below for an overview of the ACA provisions that are affected by the delay, the provisions that are not affected by the delay and steps that employers are encouraged to take in 2014.

Achieving A Great Work-Life Balance

Do you find yourself struggling to find a fair balance between your work and your personal life? You are far from alone. Changes to the traditional workforce following the recent recession, have resulted in employees handling more of a workload than their roles had required in the past.

Employees who struggle to find balance between their professional and personal lives can suffer from poor work performance, stress, exhaustion, illness, and depression. Often times employees who are unhappy with the balance between their work and personal lives are likely to experience turnover in their careers. Finding a suitable balance for yourself and your employer may be easier to do than you think. Here are a few tips to get you started:

- Have a clear understanding of your professional obligations. Make sure that you are aware of what your employer expects of you and what they consider as above and beyond. Chances are some of the added stress and responsibilities that you find yourself overwhelmed with are not expectations for someone in your role.

- Find out what workplace flexibilities are available to you. Does your employer offer flex time? Do they allow employees to work remotely on occasion? Today’s workplace offers more flexibility than ever before. With the technology available, employers are able to allow more staff to work from home with the same capabilities and accountability as working in the office.

- Determine if you are working as efficiently as possible. Do you find yourself working overtime regularly? Chances are there are process improvements or delegations that could significantly cut down on your need to work over. The average worker spends as much as 28% of their day working on email! Set specific times of the day to check and respond to email, allowing you to be more efficient throughout the day. Unless your role requires you to be available after hours, consider turning off your email on mobile devices during your personal time. Remaining focused on your personal activities during your off time can help you make the most of your down time.

- Create and maintain priorities for yourself. Realize and accept that you can’t always be involved in everything. Determine work and personal life priorities and create a plan to help you accomplish those tasks before taking on additional obligations. Communicate to those around you that while you’d love to be involved in everything that’s not realistic for you right now, you are setting priorities that will allow you to dedicate yourself to certain important events or projects.

While admitting to yourself and others that you cannot do everything is difficult, the ramifications of a poor work-life balance can be far worse. Be honest with those around you about what you are available for and accept the things that you cannot handle at the moment. Remember to take time for yourself. Most positions provide vacation or personal time off, taking the time off that you have earned is important and can allow you to return to work refreshed and refocused.

Are you a stand out professional, skilled trades person, or technical professional seeking contingent, temporary, or long term career opportunities? Visit our job seekers section for more information! Want to learn more about how you can gain access to Trillium’s national network of professionals and skilled workers? Contact us today!

Trillium, a national leader in staffing and recruitment is a valued staffing partner to over 5,000 companies nationwide. Trillium is privately owned by Oskar René Poch.

2013 Health Care Reform Compliance Checklist

2013 Health Care Reform Compliance Checklist

Brought to you by Kapnick Insurance Group

In light of the Supreme Court’s June 28, 2012, decision to uphold the health care reform law, or Affordable Care Act (ACA), employers must continue to comply with ACA mandates that are currently in effect. Employers must also prepare to comply with ACA changes that will go into effect in the future. To prepare for upcoming changes, employers need to be aware of the ACA mandates that will go into effect in 2013.

This Legislative Brief provides a compliance checklist for employers for 2013. Please contact Kapnick Insurance Group for assistance or if you have questions about changes that were required in previous years.

GRANDFATHERED PLAN STATUS

A grandfathered plan is one that was in existence when health care reform was enacted on March 23, 2010. If you make certain changes to your plan that go beyond permitted guidelines, your plan is no longer grandfathered. Contact Kapnick Insurance Group if you have questions about changes you have made, or are considering making, to your plan.

- If you have a grandfathered plan, determine whether it will remain its grandfathered status for the 2013 plan year. Grandfathered plans are exempt from some of the health care reform requirements. A grandfathered plan’s status will affect its compliance obligations from year-to-year.

- If you move to a non-grandfathered plan, confirm that the plan has all of the additional patient rights and benefits required by ACA. This includes, for example, coverage of preventative care without cost-sharing requirements.

ANNUAL LIMITS

Effective for plan years beginning on or after Jan. 1, 2014, health plans will be prohibited from placing annual limits on essential health benefits. Until then, however, restricted annual limits are permitted.

- Unless a health plan received an annual limit waiver, its annual limit on essential health benefits for the 2013 plan year cannot be less than $2 million. (This limit applies to plan years beginning on or after Sept. 23, 2012, but before Jan. 1, 2014.)

SUMMARY OF BENEFITS AND COVERAGE

Health plans and health insurance issuers must provide a Summary of Benefits and Coverage (SBC) to participants and beneficiaries. The SBC is a relatively short document that provides simple and consistent information about health plan benefits and coverage in plain language. A template for the SBC is available, along with instructions and examples, and a uniform glossary of terms.

Plans and issuers must provide the SBC to participants and beneficiaries who enroll or re-enroll during an open enrollment period beginning with the first open enrollment period that begins on or after Sept. 23, 2012. The SBC also must be provided to participants and beneficiaries who enroll other than through an open enrollment period (including individuals who are newly eligible for coverage and special enrollees) effective for plan years beginning on or after Sept. 23, 2012.

□ If your plan has an open enrollment period beginning on or after Sept. 23, 2012, confirm that the SBC is included with the open enrollment package. For participants and beneficiaries who enroll outside of the open enrollment period, confirm that the SBC will be provided to these individuals beginning with the plan year starting on or after Sept. 23, 2012.

o If you have a self-funded plan, the plan administrator is responsible for providing the SBC.

o If you have an insured plan, both the plan and the issuer are obligated to provide the SBC, although this obligation is satisfied for both parties if either one provides the SBC. Thus, if you have an insured plan, you should work with your health insurance issuer to determine which entity will assume responsibility for providing the SBC. Please contact Kapnick Insurance Group for assistance.

60-DAY NOTICE OF PLAN CHANGES

A health plan or issuer must provide 60 days’ advance notice of any material modifications to the plan that are not related to renewals of coverage. Notice can be provided in an updated SBC or a separate summary of material modifications. This 60-day notice requirement becomes effective when the SBC requirement goes into effect for a health plan.

PREVENTIVE CARE SERVICES FOR WOMEN

Effective for plan years beginning on or after Aug. 1, 2012, non-grandfathered health plans must cover specific preventive care services for women without cost-sharing requirements.

□ The covered preventive care services for women include: well-woman visits; gestational diabetes screening; human papillomavirus (HPV) testing; sexually transmitted infection (STI) counseling; human immunodeficiency virus (HIV) screening and counseling; FDA-approved contraception methods and contraceptive counseling; breastfeeding support, supplies and counseling; and domestic violence screening and counseling.

□ Exceptions to the contraception coverage requirement apply to certain religious employers. The preventive care guidelines for women are available at: www.hrsa.gov/womensguidelines/.

$2,500 Contribution Limit for Health FSAs

Effective for plan years beginning on or after Jan. 1, 2013, an employee’s annual pre-tax salary reduction contributions to a health flexible spending account (FSA) must be limited to $2,500. (The $2,500 limit will be indexed for cost-of-living adjustments for 2014 and later years.)

Health FSA plan sponsors are free to impose an annual limit that is lower than the ACA limit for employees’ health FSA contributions. Also, the $2,500 limit does not apply to employer contributions to the health FSA and it does not impact contributions under other employer-provided coverage. For example, employee salary reduction contributions to an FSA for dependent care assistance or adoption care assistance are not affected by the $2,500 health FSA limit.

W-2 REPORTING

Beginning with the 2012 tax year, employers that are required to issue 250 or more W-2 Forms must report the aggregate cost of employer-sponsored group health coverage on employees’ W-2 Forms. The cost must be reported beginning with the 2012 W-2 Forms, which are issued in January 2013.

□ ACA’s W-2 reporting requirement is optional for smaller employers until further guidance is issued. Also, the reporting is for informational purposes only; it does not affect the taxability of benefits.

RETIREE DRUG SUBSIDY

The Medicare Part D program includes a Retiree Drug Subsidy (RDS) to encourage employers to continue providing prescription drug coverage to Medicare-eligible retirees. The RDS is available to certain employers that sponsor group health plans covering retirees who are entitled to enroll in Medicare Part D but elect not to do so. Employers receive RDS payments tax-free. In addition, before 2013, employers receiving the RDS could take a tax deduction for their retiree prescription drug costs, unreduced for the subsidy amount.

□ Beginning in 2013, employers receiving the RDS will no longer be permitted to take a tax deduction for the subsidy amount.

MEDICARE TAX INCREASES

Effective Jan. 1, 2013, the Medicare Part A (hospital insurance) tax rate increases by 0.9 percent (from 1.45 percent to 2.35 percent) on wages over $200,000 for an individual taxpayers and $250,000 for married couples filing jointly. (The tax is also expanded to include a 3.8 percent tax on unearned income in the case of individual taxpayers earning over $200,000 and $250,000 for married couples filing jointly).

□ An employer must withhold the additional Medicare tax on wages or compensation it pays to an employee in excess of $200,000 in a calendar year. An employer has this withholding obligation even though an employee may not be liable for the additional Medicare tax because, for example, the employee’s wages or other compensation together with that of his or her spouse (when filing a joint return) does not exceed the $250,000 liability threshold. Any withheld additional Medicare tax will be credited against the total tax liability shown on the individual’s income tax return (Form 1040).

EMPLOYEE NOTICE OF EXCHANGE

Employers will be required to provide all new hires and current employees with a written notice about ACA’s health insurance exchanges (Exchanges). ACA required employers to provide the Exchange notice by March 1, 2013, but the DOL delayed this deadline.

□ On May 8, 2013, the DOL set a compliance deadline for providing the Exchange notices that matches up with the start of the first open enrollment period under the Exchanges, as follows:

· New Hires – Employers must provide the notice to each new employee at the time of hiring beginning Oct. 1, 2013. For 2014, the DOL will consider a notice to be provided at the time of hiring if the notice is provided within 14 days of an employee’s start date.

· Current Employees – With respect to employees who are current employees before Oct. 1, 2013, employers are required to provide the notice no later than Oct. 1, 2013.

□ In general, the notice must:

· Inform employees about the existence of the Exchange and give a description of the services provided by the Exchange;

· Explain how employees may be eligible for a premium tax credit or a cost-sharing reduction if the employer’s plan does not meet certain requirements;

· Inform employees that if they purchase coverage through the Exchange, they may lose any employer contribution toward the cost of employer-provided coverage, and that all or a portion of the employer contribution to employer-provided coverage may be excludable for federal income tax purposes; and

· Include contact information for the Exchange and an explanation of appeal rights.

□ The DOL also provided model Exchange notices for employers to use, which will require some customization. The notice may be provided by first-class mail, or may be provided electronically if the requirements of the DOL’s electronic disclosure safe harbor are met. Federal agencies plan to issue more specific guidance on this notice requirement.

PCORI FEES

ACA created the Patient-Centered Outcomes Research Institute (Institute) to help patients, clinicians, payers and the public make informed health decisions by advancing comparative effectiveness research. The Institute’s research is to be funded, in part, by fees paid by health insurance issuers and sponsors of self-insured health plans. These research fees are called Patient-Centered Outcomes Research Institute fees (PCORI fees), although they may also be called PCOR fees or comparative effectiveness research (CER) fees.

□ Self-funded plans and health insurance issuers must pay a $1 per covered life fee for comparative effectiveness research. Fees increase to $2 the next year and will be indexed for inflation after that.

□ Fees are effective for plan years ending on or after Oct. 1, 2012. Full payment of the research fees will be due by July 31 of each year. It will generally cover plan years that end during the preceding calendar year. Thus, the first possible deadline for paying the CER fees is July 31, 2013.

HIPAA CERTIFICATION

Health plans must file a statement with the Department of Health and Human Services (HHS), certifying their compliance with HIPAA’s electronic transaction standards and operating rules. Under ACA, the first deadline for certifying compliance with certain HIPAA standards and rules is Dec. 31, 2013. HHS has indicated that it intends on issuing more guidance on this requirement in the future.

![]() This Legislative Brief is not intended to be exhaustive nor should any discussion or opinions be construed as legal advice. Readers should contact legal counsel for legal advice.

This Legislative Brief is not intended to be exhaustive nor should any discussion or opinions be construed as legal advice. Readers should contact legal counsel for legal advice.

© 2012 Zywave, Inc. All rights reserved. 10/12; BK 5/13